There are dozens of different strategies that you can adopt when investing in real estate, but generally speaking, there are two different philosophies or mindsets.

Short-term real estate investing and long-term real estate investing.

Both of these mindsets can result in big gains for property investors, but there are certainly differences when it comes to risk management, personal investment, and quite frankly - how stressful the whole process can be.

The good news is that you don't need to commit to one or the other, and you could have a real estate investment portfolio with properties that are selected for the short term and others that have been selected for their long-term capital growth potential.

But is one of these mindsets superior to the other when it comes to real estate investing?

Let's find out.

Your real estate investment isn't likely to increase much in less than a year, and as a short-term investor, you need to overcome this obstacle.

Often known as the "fix and flip" method, renovating for short-term gain involves selecting an investment property, making some smart renovations to add value, and selling it for a tidy profit.

It sounds simple, but a huge body of work goes into selecting the right property, making the right renovations, navigating council approvals, and overcoming those high entry and exit costs.

As a rule of thumb, you should aim to add $3 to your investment property for every $1 you spend. To maximise your ROI, focus on the bathroom, kitchen, and laundry. Smart, cost-friendly renovations like ripping up carpet to expose natural floorboards or a fresh coat of paint indoors can also go a long way to adding value. Landscaping and outdoor living upgrades should also be considered - especially at the front of the property (remember, first impressions count!)

Some other things to consider for a fix and flip strategy include:

Strategies that focus on rental yield are usually longer-term strategies, but some investors approach rentals with a short-term mindset.

For example, if you own a property in a coastal or beachside area where demand regularly skyrockets, it might be worth pursuing a short-term rental strategy where occupants sign leases for weeks or months at a time - not years. That way, you can ensure your property is free for renters with deep pockets during the holiday season.

Short-term rentals can generate much higher profits during peak season, and a shorter occupancy time makes it easy for you to have the property professionally cleaned and maintained regularly, helping to keep it in good condition.

As well as flexibility and greater earning potential, short-term rentals also allow property owners to use the investment property themselves if required. The end of the current rental period is never too far away, making it easy for you to plan a holiday of your own once in a while!

Of course, this Airbnb-style approach to renting is highly situational, and you need to own the right type of property in the right sort of location. But if you are in a position to pursue a short-term rental strategy, it may be worth its weight in gold. And the best part about it is that you can reap the benefits of short-term investing while retaining your asset and repeating the strategy for years and years.

The short-term approach to property development is much like the renovation strategy mentioned above. You buy a property or block of land and develop it to add as much value to your purchase as possible.

You could subdivide and build multiple townhouses, keep the existing property and build a new detached house on the remaining land, or buy a block that has already been approved for specific property development projects - plans and all!

Once the project is complete, you can sell your developments, pay off your loans, pocket the profits (minus taxes), and move on to your next project.

An even more stripped-back approach to property development is simply purchasing a large, vacant block, subdividing that land into multiple blocks, and selling the land for a higher price per square metre. You might have paid $800k for a 1,000m² block, but if you can sell four 250m² blocks for $300k each, that's $400k in your pocket. Selling smaller blocks of land for a lower price will also attract more buyers, meaning more competition and more opportunities to drive up prices.

Of course, you will need to consider capital gains taxes, stamp duty, the selling agent's commission, and other costs that will eat into your profits. Compared to the renovation approach, there will be more focus on the land and less on the house for development projects - especially if you plan on buying a vacant block or bulldozing any existing structures. It's important to understand what you can and cannot build on the land, considering council bylaws, overlays, easements, covenants, and any other restrictions that may prevent your block of land from reaching its full potential.

Property development (and all the approvals and processes involved) take time, so this might not be the shortest of short-term strategies. For most projects I work on, there’s about a 2-year process from when you first purchase the development site to when you sell your developed properties. But as long as you manage the development costs, turning one property into two, or one block into five can be a profitable short-term strategy.

The "buy and hold" method essentially involves purchasing an investment property, waiting for it to appreciate as the years go on, and eventually selling it for a tidy profit. This approach involves chasing capital gains by selecting a property with ongoing appeal and growing demand.

You don't need to renovate to add extra value, and you don't need to rent the property out to take advantage of rental yield (although, you can do both these things as part of your buy-and-hold strategy if you choose). Just sit back, relax, and use a negative gearing strategy to offset your expenses and lower your taxable income if necessary.

If you don't want to sell the property, you can take an even longer-term approach. Assuming your property has increased in value as planned, you can leverage the equity and use those funds to purchase your next investment property - double the assets, double the gains.

If you were attempting a short-term "buy and hold" strategy, the timing would become extremely important. If you are not giving your property years to appreciate, you need to try and buy at the lowest point of the cycle and sell at the highest point.

Timing is still a factor for longer-term "buy and hold" strategies, but if you have all the fundamentals in place, then the years your property has had to appreciate will mean you're still making a great profit, even if you sell when the market is a bit flat. But hey, you've held the property for this long - why not wait a little bit longer?!

As I mentioned above, you can always combine a "buy and hold" method with a rental yield strategy. Properties that are good candidates for capital growth are often also suitable for producing plenty of rental income. Look for homes in strong or emerging neighbourhoods and consider things like school zones, population growth, nearby amenities, proximity to universities, hospitals and other high-wage industries, and overall changes in the job market.

If your investment property is positively geared, it's generating more money in rental income than what it costs to upkeep the property. You can then use that extra income to fund your next investment or any other expenses. If your rental income isn't making you enough money, you can still take advantage of the tax benefits associated with negative gearing.

Long-term rentals are much more common than short-term rentals. Some things to consider when pursuing a long-term rental strategy include:

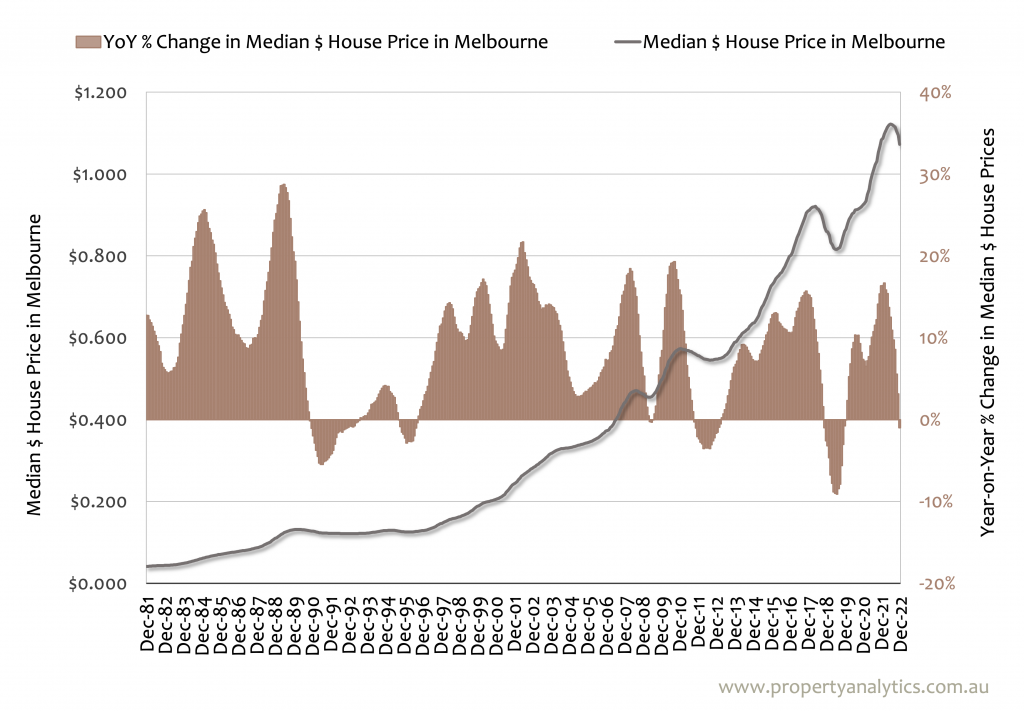

As investment consultants and buyers advocates serving Fitzroy and the wider Melbourne area, the team at Property Analytics can help you understand the pros and cons of long-term rental property strategies. While rental yield is a useful tool for property investors, we would not recommend prioritising it at the expense of capital growth.

For example, you may find a property with some appeal for renters, but you should also focus on the land and how this may contribute to the value of your investment over time. The endgame for any asset - even a rental property - is selling it for profit, so it pays to set yourself up for long-term success.

Land banking is essentially the "buy and hold" method except it skips the property altogether and focuses on acquiring blocks of land or undeveloped farmland. The idea is that you sit on this land for years - maybe even decades - while you wait for it to appreciate in value. Land is a limited resource, and eventually, you may be able to sell your investment to an aspiring home builder, a big developer, or maybe even a fellow investor for a tidy profit. Theoretically, there will be little to no maintenance costs for owning a block of land, but loan repayments, interest, land taxes, and council taxes can still apply.

Land banking still comes with its risks though, especially if you are buying undeveloped land that may not be zoned or approved for development for many years. Be aware of land banking schemes and scams, and make sure you do your research before buying an empty block of land.

We've already talked about property development as a short-term investment option, and many of the same points apply.

Your aim is to buy a property or block of land and develop it to its full potential. That could take the form of multiple townhouses, a duplex project, or even just a vacant block of land that you subdivide.

The difference here is that you don't sell your development as soon as construction is complete. Instead, you hold onto the property for the long term and take advantage of all the benefits that come with it.

You could enjoy high rental yields from multiple brand-new properties, take advantage of depreciation tax benefits over time, refinance your property to access extra funds for your next development, and watch the strong capital growth roll in.

If you've done it all properly, that project that you poured so much time, money, and effort into is now a valuable long-term asset. You could cash in and enjoy the short-term wins, but it often makes more sense to retain your asset and reap the longer-term benefits.

If you're wondering whether long-term investing or short-term investing is better, you're asking the wrong question.

Some better questions to ask would be "what should I look for in an investment property?" or "how can I grow my real estate portfolio?" Basically, whether you want to invest in real estate for the short-term or the long-term, you need to know how to do it well.

That's where Property Analytics comes in.

My team can help you put a strategy in place, find the perfect property or development site, and help you close the deal through expert negotiations.

Based in Ivanhoe, we're buyers advocates serving Kew East and all Melbourne suburbs. That means we're experts in shortlisting suburbs and properties and buying investments on your behalf.

We're also property investment advisers and development consultants in Melbourne. That means the properties we select are built around your financial goals and investment strategy. From detailed feasibility studies to putting all your development plans in place, Property Analytics takes care of the whole process.

All our services are backed by valuable market research that we not only have access to but have personally cultivated over the last decade. Our real estate analysts have their fingers on the pulse of emerging trends and historical data, and some of the largest, most successful industry professionals subscribe to our database. When you partner with Property Analytics, we put that data to work for you.

Become a master of real estate investing in the short-term and the long-term. Get to know Property Analytics and talk to us about your investment goals.