October 21, 2024

October 21, 2024

When it comes to making an investment count, there are many factors at play. One of the most undervalued yet underrated aspects of the entire process is, without a doubt, market analysis. If the ever-changing Melbourne housing market, you should never underestimate the power of thorough market analysis and research. Whether you’re a first-time buyer […]

READ MORE October 2, 2024

October 2, 2024

If you’re pursuing an investment or simply following the news, you’ll be well aware of how topsy-turvy Melbourne’s real estate market can be. However, there are experts available to help. As an investor, one of the most valuable partnerships you can make is with a dedicated property development consultant. Whether it’s a high-rise in the […]

READ MORE September 16, 2024

September 16, 2024

Rental prices have boomed across Melbourne over the last 2+ years. The graph below shows overall asking rents are up 40%% for units, while Melbourne’s Inner City has seen an increase of 60%. When combined with remarkably low vacancy rates, the current supply-demand balance in Melbourne is scary. If we cast our minds back even […]

READ MORE July 30, 2024

July 30, 2024

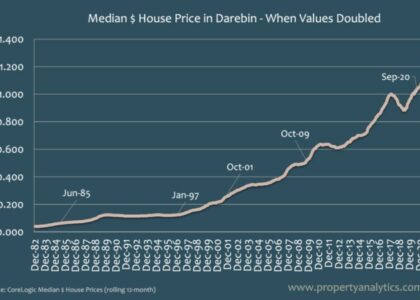

Darebin is a Council Area in Melbourne’s North that trends pretty closely to the city’s property market as a whole. The graph below illustrates how house prices have doubled in value over the past four decades. It’s taken anywhere between 3 to 10 years for prices to double. Three further insights jump out from this […]

READ MORE June 18, 2024

June 18, 2024

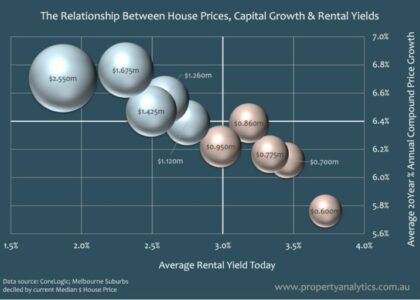

This is a really common question. The answer? In part, it all depends on what you prioritise more – capital growth or rental yield. We know instinctively that higher priced suburbs tend to achieve greater capital growth over time, but they also tend to deliver lower rental yields. Until now, we’ve struggled to convey this […]

READ MORE May 10, 2024

May 10, 2024

Entering the property market or expanding your portfolio can be complicated. There’s a lot to understand, and for new investors, there’s certainly a lot to consider. From keeping track of property markets to the average value of suburbs, the future outlook is difficult enough for real estate professionals, let alone individual property investors. Thankfully, there […]

READ MORE May 10, 2024

May 10, 2024

A snapshot of growth areas, rental dynamics, and population-driven demand.

READ MORE April 23, 2024

April 23, 2024

Rental prices have boomed across Melbourne over the last 2 years. The below graph shows overall Asking Rents are up 28% for Units. Melbourne Inner City has increased twice as much. It wasn’t long ago that many predicted high vacancy rates for years to come. So many cafes, bars, and restaurants were brought to their […]

READ MORE April 23, 2024

April 23, 2024

Darebin is a Council Area in Melbourne’s north that trends pretty closely to overall Melbourne market. The below graph shows when House Prices doubled in value over the last 4 decades. It’s taken anywhere between 3 to 10 years for prices to double. Three further insights jump out from this graph: Another way to view […]

READ MORE April 19, 2024

April 19, 2024

A deep dive into the relationship between a property developer and a buyer’s agent.

READ MORE April 12, 2024

April 12, 2024

Boost property development success by partnering with a buyer’s agent.

READ MORE April 3, 2024

April 3, 2024

Investing in property provides avenues for wealth accumulation and supplementary income, particularly when approached strategically and with expert guidance.

READ MORE