March 24, 2026

March 24, 2026

Did you know that Melbourne’s property market is expected to rise to pre-pandemic highs later this year? In fact, some analysts predict house prices will climb as much as 6.6% by the end of 2026,(Source: Property Update). Chances are, you may have already seen, heard, or experienced this rise first hand. If you’re already at […]

READ MORE February 20, 2026

February 20, 2026

Melbourne is a vibrant place, a city that is growing and expanding. It is a city ripe for investors, if you know where to look. You might hear on the news, or read about ‘growth corridors’ or new builds, but do you understand what that means? Are these really the best places to invest your […]

READ MORE January 16, 2026

January 16, 2026

As we enter 2026, Melbourne house prices have just hit another record high (Source: Sydney Morning Herald). In December, the median price reached a staggering figure of $1.11 million. Throw in the added competition from investors, overseas buyers, and recent changes to the first-home buyer deposit scheme, and it’s safe to say things are pretty […]

READ MORE December 23, 2025

December 23, 2025

From rental yields to capital growth, property investment opens the door to opportunities many people never imagined, but success doesn’t just come from being first to the post. With a real estate market that’s changing day to day, doing your due diligence has never been so important, and we can’t drive home this point enough. […]

READ MORE November 28, 2025

November 28, 2025

This October, nearly 2000 Melbourne properties were put up for auction in a single week (Source: REA Group). Although spring is widely known as a popular time to sell a home, these figures show that, as a means of selling, auctions are as popular as ever. The question is this: how exactly can you beat […]

READ MORE November 22, 2024

November 22, 2024

I bought a property for a client the other weekend with a simple but effective auction strategy: Quietly study the competition until bidding hits the reserve, wait for things to slow down a bit, and then bid hard. Every property, campaign, and auction is different, so this isn’t a one-size fits all approach (i.e., I […]

READ MORE October 21, 2024

October 21, 2024

When it comes to making an investment count, there are many factors at play. One of the most undervalued yet underrated aspects of the entire process is, without a doubt, market analysis. If the ever-changing Melbourne housing market, you should never underestimate the power of thorough market analysis and research. Whether you’re a first-time buyer […]

READ MORE June 18, 2024

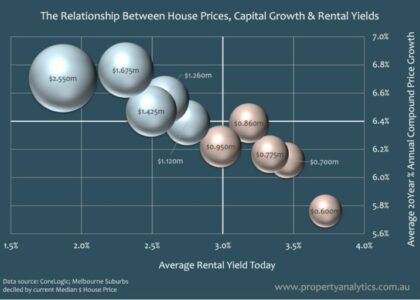

June 18, 2024

This is a really common question. The answer? In part, it all depends on what you prioritise more – capital growth or rental yield. We know instinctively that higher priced suburbs tend to achieve greater capital growth over time, but they also tend to deliver lower rental yields. Until now, we’ve struggled to convey this […]

READ MORE April 11, 2025

April 11, 2025

A lot of investment opportunities look great on paper, but not every development is what it appears to be–especially when it’s put under the microscope. So, how exactly can you tell if a townhouse development is worth your time or fraught with potential risks? The answer is a comprehensive feasibility study that analyses every fine […]

READ MORE September 24, 2025

September 24, 2025

Still struggling to break down the barriers and find the right home? You might not be using the right strategy–that’s to say, it’s unlikely you’ve been using all the tools at your disposal. At Property Analytics, our buyer’s agents have helped countless homebuyers to both identify and avoid costly mistakes. Keen to learn how? Let’s […]

READ MORE October 29, 2025

October 29, 2025

What’s the best Melbourne suburb to invest in? Is it north of the river, near the Dandenongs, on the Peninsula, or somewhere out west? Finding the right pocket of the city is hard enough, let alone narrowing it down to a specific suburb–so why not lean on the advice of an industry expert! In this […]

READ MORE August 26, 2025

August 26, 2025

With Spring rapidly approaching, there’s about to be a flurry of open listings and inspections across the city of Melbourne. If you’re unprepared, it’s all too easy to get overwhelmed, outgunned, or stuck with a property with long-term issues. Fortunately, finding the right property isn’t something you have to go through alone. At Property Analytics, […]

READ MORE